Videos

Cost Data for Managerial Purposes—Finding Unknowns

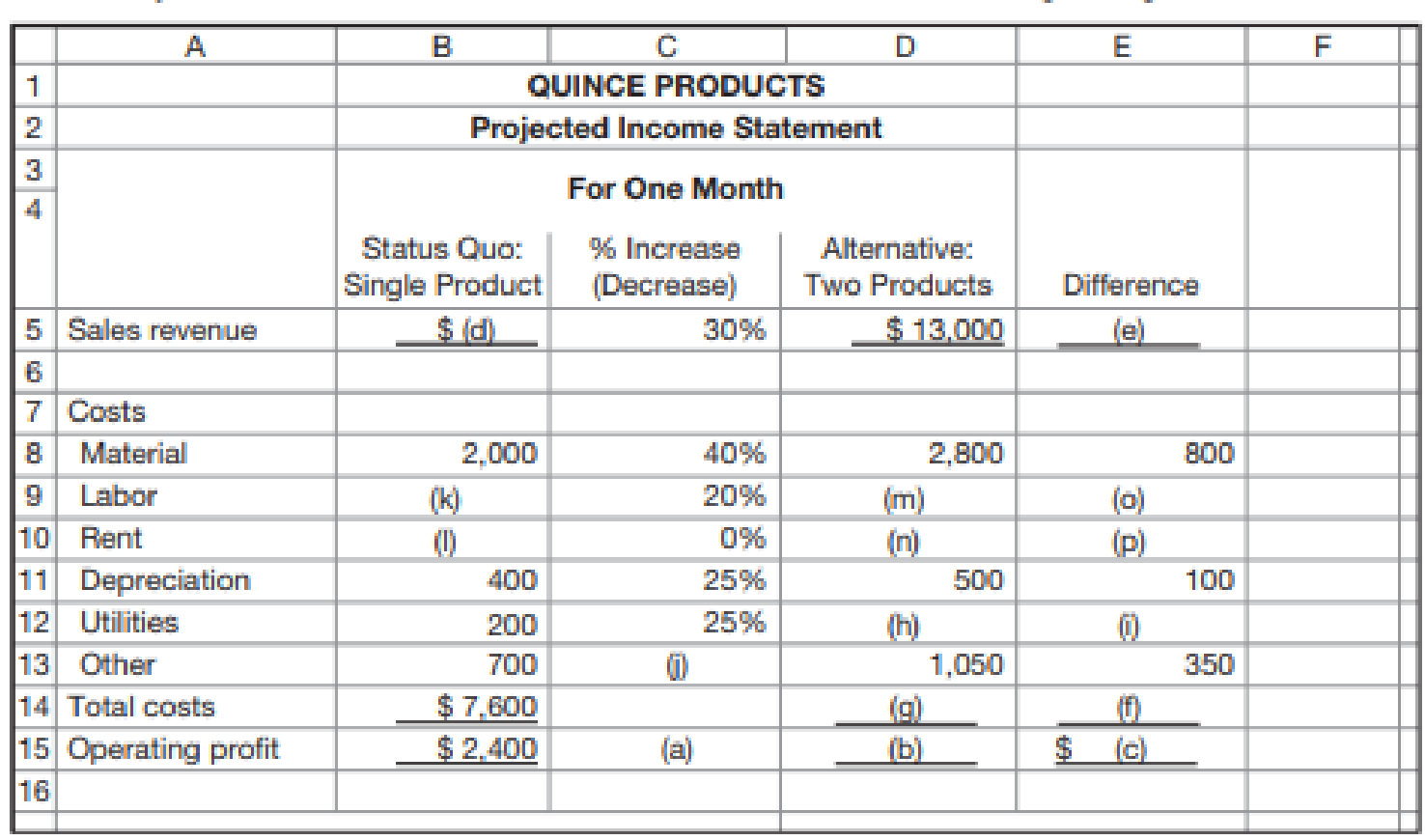

Quince Products is a small company in southern California that makes jams and preserves. Recently, a sales rep from one of the company’s suppliers suggested that Quince could increase its profitability by 50 percent if it introduced a second line of products, packaged fruit. She offered to do the analysis and show the company her assumptions.

When Quince’s management opened the spreadsheet sent by the sales rep, they noticed that there were several blank cells. In the meantime, the sales rep had taken a job with a competitor and told the managers at Quince that she could no longer advise them. Although they were not sure they should rely on the analysis, they asked you to see if you could reconstruct the sales rep’s analysis. They had been considering this new business already and wanted to see if their analysis was close to that of an outside observer. The incomplete spreadsheet follows.

Required

Fill in the blank cells.

Fill in the blank cells of the projected income statement.

Explanation of Solution

Projected income statement: The projected income statement represents the future financial position of the entity. The projected income statement is prepared with an objective of showing the financial results for a future period of time.

Fill in the blank cells of the projected income statement:

| Company Q | ||||

| Projected Income Statement | ||||

| For One Month | ||||

| Status Quo: | % Increase | Alternative | ||

| Single Product | Decrease | Two Products | Difference | |

| Sales revenue | $ 10,000 (d) | 30% | $ 13,000 | $ 3,000 (e) |

| Costs | ||||

| Material | $ 2,000 | 40% | $ 2,800 | $ 800 |

| Labor | $ 2,500 (k) | 20% | $ 3,000 (m) | $ 500 (o) |

| Rent | $ 1,800 (l) | 0% | $ 1,800 (n) |

|

| Depreciation | $ 400 | 25% | $ 500 | $ 100 |

| Utilities | $ 200 | 25% | $ 250 (h) | $ 50 (i) |

| Other | $ 700 | 50% (j) | $ 1,050 | $ 350 |

| Total costs | $ 7,600 | $ 9,400 (g) | $ 1,800 (f) | |

| Operating profit | $ 2,400 (a) | $ 3,600 (b) | $ 1,200 (c) | |

Working note 1:

Compute value of (a):

It is given that the profit has increased by 50%, (a) represent the % increase or decrease in profit.

Working note 2:

Compute value of (b):

Working note 3:

Compute value of (c):

Working note 4:

Compute value of (d):

Working note 5:

Compute value of (e):

Working note 5:

Compute value of (f):

Working note 6:

Compute value of (g):

Working note 6:

Compute value of (h):

Working note 7:

Compute value of (i):

Working note 8:

Compute value of (j):

Working note 8:

Compute value of (k):

Labor plus rent (single product):

Labor plus rent (two products):

Increase in labor:

Thus,

Working note 8:

Compute value of (l):

Working note 8:

Compute value of (m):

Working note 9:

Compute value of (n):

Working note 10:

Compute value of (o):

Working note 11:

Compute value of (p):

Want to see more full solutions like this?

Chapter 1 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Henrys Cafe is a local restaurant that is growing quickly. While the company does not yet have a balanced scorecard, Henry has mentioned that being efficient in producing meals is a high priority of his business and appears to be a significant driver of profits. Henry tells you he gathers the following data: sales, cost of labor, employee turnover, labor hours, cost of ingredients, overhead costs, average training hours per employee, number of erroneous meals prepared, the time when orders were made (e.g., at 12:43 PM), the time when orders were delivered, and number of customers per day. a. Under which performance perspective on the balanced scorecard should Henrys strategic objective to efficiently produce meals be placed? b. Based on the data collected, what are at least three performance metrics Henry could develop to measure his strategic objective to efficiently produce meals? c. Identify whether the performance metrics you suggested in part (b) are leading or lagging indicators relative to a performance metric total cost of production per meal.arrow_forwardAt the beginning of the last quarter of 20x1, Youngston, Inc., a consumer products firm, hired Maria Carrillo to take over one of its divisions. The division manufactured small home appliances and was struggling to survive in a very competitive market. Maria immediately requested a projected income statement for 20x1. In response, the controller provided the following statement: After some investigation, Maria soon realized that the products being produced had a serious problem with quality. She once again requested a special study by the controllers office to supply a report on the level of quality costs. By the middle of November, Maria received the following report from the controller: Maria was surprised at the level of quality costs. They represented 30 percent of sales, which was certainly excessive. She knew that the division had to produce high-quality products to survive. The number of defective units produced needed to be reduced dramatically. Thus, Maria decided to pursue a quality-driven turnaround strategy. Revenue growth and cost reduction could both be achieved if quality could be improved. By growing revenues and decreasing costs, profitability could be increased. After meeting with the managers of production, marketing, purchasing, and human resources, Maria made the following decisions, effective immediately (end of November 20x1): a. More will be invested in employee training. Workers will be trained to detect quality problems and empowered to make improvements. Workers will be allowed a bonus of 10 percent of any cost savings produced by their suggested improvements. b. Two design engineers will be hired immediately, with expectations of hiring one or two more within a year. These engineers will be in charge of redesigning processes and products with the objective of improving quality. They will also be given the responsibility of working with selected suppliers to help improve the quality of their products and processes. Design engineers were considered a strategic necessity. c. Implement a new process: evaluation and selection of suppliers. This new process has the objective of selecting a group of suppliers that are willing and capable of providing nondefective components. d. Effective immediately, the division will begin inspecting purchased components. According to production, many of the quality problems are caused by defective components purchased from outside suppliers. Incoming inspection is viewed as a transitional activity. Once the division has developed a group of suppliers capable of delivering nondefective components, this activity will be eliminated. e. Within three years, the goal is to produce products with a defect rate less than 0.10 percent. By reducing the defect rate to this level, marketing is confident that market share will increase by at least 50 percent (as a consequence of increased customer satisfaction). Products with better quality will help establish an improved product image and reputation, allowing the division to capture new customers and increase market share. f. Accounting will be given the charge to install a quality information reporting system. Daily reports on operational quality data (e.g., percentage of defective units), weekly updates of trend graphs (posted throughout the division), and quarterly cost reports are the types of information required. g. To help direct the improvements in quality activities, kaizen costing is to be implemented. For example, for the year 20x1, a kaizen standard of 6 percent of the selling price per unit was set for rework costs, a 25 percent reduction from the current actual cost. To ensure that the quality improvements were directed and translated into concrete financial outcomes, Maria also began to implement a Balanced Scorecard for the division. By the end of 20x2, progress was being made. Sales had increased to 26,000,000, and the kaizen improvements were meeting or beating expectations. For example, rework costs had dropped to 1,500,000. At the end of 20x3, two years after the turnaround quality strategy was implemented, Maria received the following quality cost report: Maria also received an income statement for 20x3: Maria was pleased with the outcomes. Revenues had grown, and costs had been reduced by at least as much as she had projected for the two-year period. Growth next year should be even greater as she was beginning to observe a favorable effect from the higher-quality products. Also, further quality cost reductions should materialize as incoming inspections were showing much higher-quality purchased components. Required: 1. Identify the strategic objectives, classified by the Balanced Scorecard perspective. Next, suggest measures for each objective. 2. Using the results from Requirement 1, describe Marias strategy using a series of if-then statements. Next, prepare a strategy map. 3. Explain how you would evaluate the success of the quality-driven turnaround strategy. What additional information would you like to have for this evaluation? 4. Explain why Maria felt that the Balanced Scorecard would increase the likelihood that the turnaround strategy would actually produce good financial outcomes. 5. Advise Maria on how to encourage her employees to align their actions and behavior with the turnaround strategy.arrow_forwardThe Chocolate Baker specializes in chocolate baked goods. The firm has long assessed the profitability of a product line by comparing revenues to the cost of goods sold. However, Barry White, the firms new accountant, wants to use an activity-based costing system that takes into consideration the cost of the delivery person. Following are activity and cost information relating to two of Chocolate Bakers major products: Using activity-based costing, which of the following statements is correct? a. The muffins are 2,000 more profitable. b. The cheesecakes are 75 more profitable. c. The muffins are 1,925 more profitable. d. The muffins have a higher profitability as a percentage of sales and, therefore, are more advantageous.arrow_forward

- The Lockit Company manufactures door knobs for residential homes and apartments. Lockit is considering the use of simple (single-driver) and multiple regression analyses to forecast annual sales because previous forecasts have been inaccurate. The new sales forecast will be used to initiate the budgeting process and to identify more completely the underlying process that generates sales. Larry Husky, the controller of Lockit, has considered many possible independent variables and equations to predict sales and has narrowed his choices to four equations. Husky used annual observations from 20 prior years to estimate each of the four equations. Following are definitions of the variables used in the four equations and a statistical summary of these equations: St=ForecastedsalesindollarsforLockitinperiodtSt1=ActualsalesindollarsforLockitinperiodt1Gt=ForecastedU.S.grossdomesticproductinperiodtGt1=ActualU.S.grossdomesticproductinperiodt1Nt1=Lockitsnetincomeinperiodt1 Required: 1. Write Equations 2 and 4 in the form Y = a + bx. 2. If actual sales are 1,500,000 in the current year, what would be the forecasted sales for Lockit in the coming year? 3. Explain why Larry Husky might prefer Equation 3 to Equation 2. 4. Explain the advantages and disadvantages of using Equation 4 to forecast sales.arrow_forwardVice President for Sales and Marketing at Waterways Corporation is planning for production needs to meet sales demand in the coming year. He is also trying to determine how the company's profits might be increased in the coming year. This problem asks you to use cost-volume-profit concepts to help Waterways understand contribution margins of some of its products and decide whether to mass-produce any of them. Waterways markets a simple water control and timer that it mass-produces, Last year, the company sold 630,000 units at an average unit selling price of $4.40. The variable costs were $1,663,200, and the fixed costs were $742,896. Show Transcribed Text Margin of safety in dollars What is the margin of safety, both in dollars and as a ratio? (Round ratio to 0 decimal places, e.g. 25%.) Margin of safety ratio 3 $ Ć %arrow_forwardCompany XYZ is specialized in producing and selling smart watches. The company currently has two products and is planning to improve it profits in the coming years. The company is thinking of introducing a sales commission to encourage its sales people to make more sales and improve company's profitability. When designing the sales commission the company should base the sales commission on: a. The number of employees b. None of the given answers c. The contribution margin d. The selling price e. The color of the productarrow_forward

- A new product is being designed by an engineering team at Golem Security. Several managers and employees from the cost accounting department and the marketing department are also on the team to evaluate the product and determine the cost using a target costing methodology. An analysis of similar products on the market suggests a price of $132.00 per unit. The company requires a profit of 0.20 of selling price. How much is the target cost per unit? Round to two decimal places.arrow_forwardStylish Sitting is a retailer of office chairs located in San Francisco, California. Due to increased market competition, the CFO of Stylish Sitting has grown worried about the firm's upcoming income stream. The CFO asked you to use the company financial information provided below. Sales price $ 73.00 Per-unit variable costs: Invoice cost 40.45 Sales commissions 17.45 Total per-unit variable costs $ 57.90 Total annual fixed costs: Advertising $ 54,500 Rent 77,000 Salaries 225,000 Total annual fixed costs $ 356,500 If 38,900 office chairs were sold, Stylish Sitting's operating income (πB) would be: (Do not round intermediate calculations.) Multiple Choice $230,890. $270,890. $200,890. $330,890.arrow_forwardColumbus Inc. sells a high end hair dryer in a super competitive marketplace. As a result, market research and competitive pressures influence the determination of their selling price. Their marketing department has done a comprehensive analysis and It looks like a price of $61 would be appropriate given the present business environment. The company has a goal of earning $30 on each unit. What is the target unit cost of each hair dryer? Enter your answers without dollar signs or commas. ASUS 13 f4 E3 X 19 OLF 11 (12 3. & 4. 5 7. 8. E T. Y. F G H K t6 立arrow_forward

- Valencia Manufacturing Company manufactures and sells musical gadgets. You have just begun your summer internship at Valencia Manufacturing. To expand sales, the business is considering paying a commission to its sales team. You have been asked to compute 1) the new break-even sales figure, and 2) the operating profit if sales increase by 10% under the new sales commission plan. She is confident that you can handle the task, because you learned CVP analysis in your accounting class. The following data was obtained: Selling price per unit Variable expenses per unit: $200 $40 $32 $18 Direct Material Direct Labour Variable Manufacturing Overhead Fixed expenses: Fixed Manufacturing Overhead Fixed Selling Costs Fixed Administrative Costs $190,000 $115,000 $135,000 6,000 Units Production/Sales After collecting your data, you performed your analysis and submitted a memo to your manager, who was very pleased with the work done, Your report indicated that the new sales commission plan would…arrow_forwardValencia Manufacturing Company manufactures and sells musical gadgets. You have just begun your summer internship at Valencia Manufacturing. To expand sales, the business is considering paying a commission to its sales team. You have been asked to compute 1) the new break-even sales figure, and 2) the operating profit if sales increase by 10% under the new sales commission plan. She is confident that you can handle the task, because you learned CVP analysis in your accounting class.The following data was obtained:Selling price per unit $200 Variable expenses per unit: Direct Material $40Fixed expenses:Production/SalesDirect Labour $32 Variable Manufacturing Overhead $18Fixed Manufacturing Overhead Fixed Selling CostsFixed Administrative Costs$190,000 $115,000 $135,0006,000 Units Find the break-even in sales find the operating profit before and after the fixed cost adjustmentsarrow_forwardNorthwind Corporation is a small information-systems consulting firm that specializes in helping companies implement standard sales-management software. The market for Northwind's services is very competitive. To compete successfully, Northwind must deliver quality service at a low cost. Northwind presents the following data for 2011 and 2012. Northwind follows a cost leadership strategy in 2012. 2011 2012 1. Number of jobs billed 70 100 2. Selling price per job $56,000 $50,000 3. Software-implementation labor-hours 35,000 38,000 4. Cost per software-implementation labor-hour $62 $65 5. Software-implementation support capacity (number of jobs it can do) 125 125 6. Total cost of software-implementation support $475,000 $525,000 7. Software-implementation support-capacity cost per job (row 6 / row 5) $3,800 $4,200 Software-implementation labor-hour costs are variable costs.…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub